I made two simplistic TensorFlow (1.x) notebooks for the benefit of my students at Copenhagen University, to demonstrate how vanilla neural nets (deeply) learn pricing of European calls and high dimensional basket options, together with a comparison with conventional polynomial regression models (a la LSM) and a quick, simple introduction to the implementation of deep learning models in TensorFlow.

Some (much) more advanced considerations for efficiently learning prices of trading books, including “twin” neural nets who learn values and risks, and the super efficient differential regularization, are found here: deep-analytics.org

Back in March, I gave a series of lectures at Kings College London on automatic adjoint differentiation, backpropagation and machine learning, and how it all connects and applies to risk management of financial derivatives.

The lectures were recorded and made freely available online, either from Kings own page:

We had another fantastic conference from QuantMinds last week in Vienna, where I was honored to chair the Numerical and Computational Finance stream. The agenda was dominated by the application of machine learning to derivatives finance.

Among many presentations focusing on big data, large infrastructures and deep neural networks, our talk stood out by a principled approach and the systematic integration and synergy of new methods from the deep learning world within the mature financial theoretical framework and in combination with other powerful financial techniques. Following Jesper Andreasen’s tradition of “computing XVA on iPad Mini”, we effectively trained small networks, within seconds to minutes, on trader workstations. We also proposed new techniques for the improvement of financial neural networks, not necessarily appropriate to other contexts, but particularly powerful for the pricing and revaluation of derivatives transactions and trading books. The most prominent of these techniques, “differential regularization”, leverages both AAD on the simulation side and back-prop on the neural side.

We extend billion thanks to our exceptional audience for a fantastic reception and feedback, to our colleagues of Danske Bank’s quantitative research for helping us polish the material and delivery, and to Danske Bank itself for encouraging and nurturing the research and development efforts necessary to properly produce game changing technologies like scripting, model hierarchies, parallel simulations, AAD and now, neural analytics.

It goes without saying that we heard other exceptional presentations, including, in my stream alone, Pierre Henry-Labordere‘s ground breaking work on the application of Schrodinger Bridges to stochastic volatility, and Jesper Andreasen’s rare and inspiring talk about scripting.

Outside of the stream, a series of filmed interviews gave me a chance to express my views on automatic differentiation (AAD), its exceptional contribution to risk management, its evolution and its future in quantitative finance combined with machine learning.

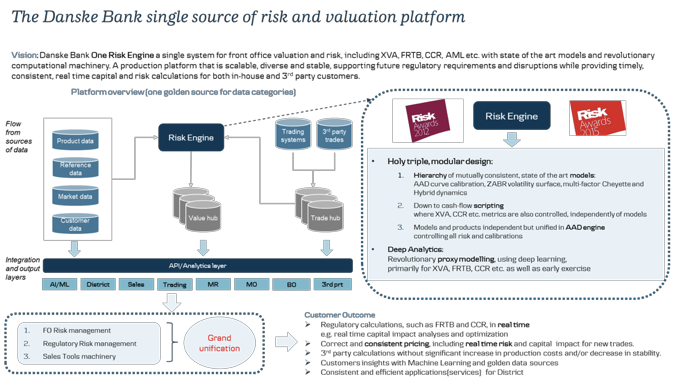

Finally, the presentation and interviews gave us an opportunity to introduce Danske Bank’s vision of “One Calculation Engine”. A core principle within Danske Bank’s quantitative research, this is a unique, single and consistent framework for the risk management of derivatives and the computation of regulations like XVA, CCR, FRTB… with the articulation of scripting, model hierarchies, parallel simulation engines, AAD and… deep analytics.

See a brief, non-technical abstract on QuantMinds page here. The 6-hour workshop is a technical one. We will discuss the mathematics of deep learning and back-propagation, and the application of AAD with implementations in Python/TensorFlow and C++. The presentation slides are found on my GitHub repo (Intro2AADinMachineLearningAndFinance.pdf), together with supplementary material: code, spreadsheets and notebooks in the folder ‘Workshop’: https://github.com/asavine/CompFinance

The event was arranged by Blanka Horvath, author of Deep Learning Volatility, where the matter of quick European option pricing in rough volatility models is resolved with deep learning methods. Thank you, Blanka.

Registration is absolutely free, but seating is limited to 40 people. I am looking forward to meet an audience interested in the most recent additions to computational finance.

This is a highly recommended reading, the best resource I could find on the subject and one of the best books I have seen on Machine Learning in general.

The complicated topic of RL is presented in an incremental, pedagogical and natural manner so that the concepts and equations flow naturally and stick in your mind. Somehow, the authors manage to teach RL in a captivating, even addictive manner without sacrificing rigor or completeness, leaving you with a fulfilling feeling of deep understanding of the subject, especially if you try to complete the numerous exercises and programming assignments. Unfortunately, solutions to exercises or assignments are not provided so readers cannot check the correctness of their understanding against the word of god (the authors), although a number of readers posted their own solutions online.