We had another fantastic conference from QuantMinds last week in Vienna, where I was honored to chair the Numerical and Computational Finance stream. The agenda was dominated by the application of machine learning to derivatives finance.

Brian Huge and I gave a talk on Deep Analytics to a vast audience of delegates, professionals and academics, including Bruno Dupire, Leif Andersen, Jesper Andreasen, Michael Dempster and many others. The room was full and some had to stand in the back for the whole 90 minutes!

Among many presentations focusing on big data, large infrastructures and deep neural networks, our talk stood out by a principled approach and the systematic integration and synergy of new methods from the deep learning world within the mature financial theoretical framework and in combination with other powerful financial techniques. Following Jesper Andreasen’s tradition of “computing XVA on iPad Mini”, we effectively trained small networks, within seconds to minutes, on trader workstations. We also proposed new techniques for the improvement of financial neural networks, not necessarily appropriate to other contexts, but particularly powerful for the pricing and revaluation of derivatives transactions and trading books. The most prominent of these techniques, “differential regularization”, leverages both AAD on the simulation side and back-prop on the neural side.

We extend billion thanks to our exceptional audience for a fantastic reception and feedback, to our colleagues of Danske Bank’s quantitative research for helping us polish the material and delivery, and to Danske Bank itself for encouraging and nurturing the research and development efforts necessary to properly produce game changing technologies like scripting, model hierarchies, parallel simulations, AAD and now, neural analytics.

It goes without saying that we heard other exceptional presentations, including, in my stream alone, Pierre Henry-Labordere‘s ground breaking work on the application of Schrodinger Bridges to stochastic volatility, and Jesper Andreasen’s rare and inspiring talk about scripting.

Outside of the stream, a series of filmed interviews gave me a chance to express my views on automatic differentiation (AAD), its exceptional contribution to risk management, its evolution and its future in quantitative finance combined with machine learning.

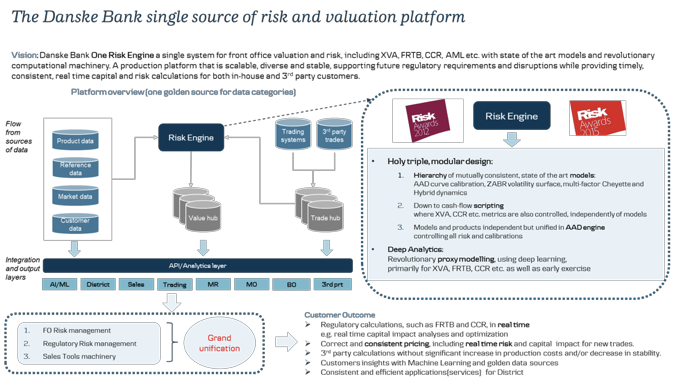

Finally, the presentation and interviews gave us an opportunity to introduce Danske Bank’s vision of “One Calculation Engine”. A core principle within Danske Bank’s quantitative research, this is a unique, single and consistent framework for the risk management of derivatives and the computation of regulations like XVA, CCR, FRTB… with the articulation of scripting, model hierarchies, parallel simulation engines, AAD and… deep analytics.

Antoine Savine, May 2019