(An excerpt from the Modern Computational Finance book)

(An excerpt from the Modern Computational Finance book)

I am working on a set of exercises and assignments for the chapters of the Modern Computational Finance book. In the meantime, interested readers will find below the final hand-in for the computational finance lecture of autumn 2018 at Copenhagen University, where the book is used as curriculum:

https://antoinesavine.com/wp-content/uploads/2019/01/compfinhandin.pdf

https://www.slideshare.net/AntoineSavine/presentations

For those of you who like my posts and stories, I am working on a few nice talks and workshops on introductory automatic differentiation, deep learning, Monte-Carlo simulations and parallel programming that will land on my SlideShare page soon. Please follow me to be notified of updates.

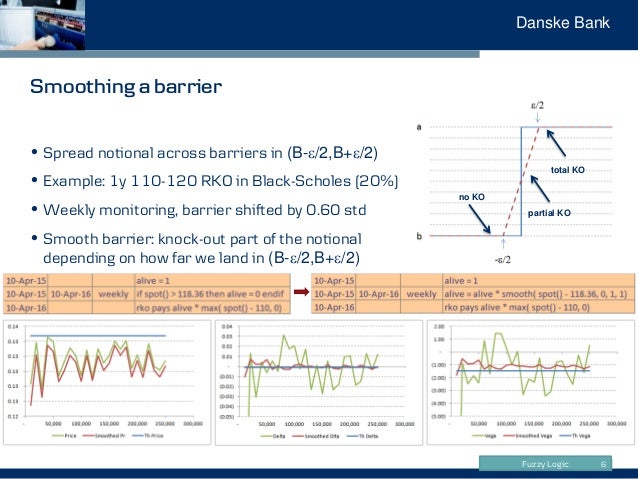

Right now, my page has my volatility lecture notes from Copenhagen University, my interest rate modeling slides from a course internal to Danske Bank, an introduction to multi-curve and collateral consistent discounting, some material on AAD and scripting, and a personal favorite about risk smoothing and fuzzy logic.

Comments, suggestions and questions are welcome, of course.

Please post your questions, suggestions, comments or reviews of the book Modern Computational Finance: AAD and Parallel Simulations on the author’s page:

https://antoinesavine.com/books-by-antoine-savine

or the book’s GoodReads page:

http://www.goodreads.com/book/show/40244920-modern-computational-finance

A public preview, including Leif Andersen’s preface, is available on SSRN:

My book is out on Amazon today. You can read about it in my Medium post:

A free preview, including Leif Andersen’s preface, is available here:

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=3281877

The companion code is freely available on GitHub:

http://github.com/asavine/CompFinance/wiki

Follow the repo to be notified of updates, extensions and fixes.

I will be answering questions, suggestions and comments on my GoodReads page:

http://www.goodreads.com/author/show/18069638.Antoine_Savine

I put all my years of promoting, teaching and professionally implementing automatic adjoint differentiation (AAD) in this book, yet it took years of working nights and week-ends to (hopefully) get it right. I hope readers find that it was worth the effort.

Antoine Savine