https://www.slideshare.net/AntoineSavine/presentations

For those of you who like my posts and stories, I am working on a few nice talks and workshops on introductory automatic differentiation, deep learning, Monte-Carlo simulations and parallel programming that will land on my SlideShare page soon. Please follow me to be notified of updates.

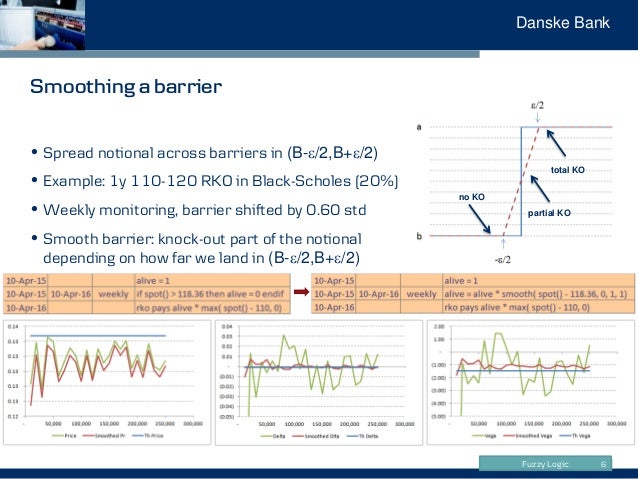

Right now, my page has my volatility lecture notes from Copenhagen University, my interest rate modeling slides from a course internal to Danske Bank, an introduction to multi-curve and collateral consistent discounting, some material on AAD and scripting, and a personal favorite about risk smoothing and fuzzy logic.

Comments, suggestions and questions are welcome, of course.