download the slides here

AAD and backpropagation in Finance, explained in 15min

download the slides here

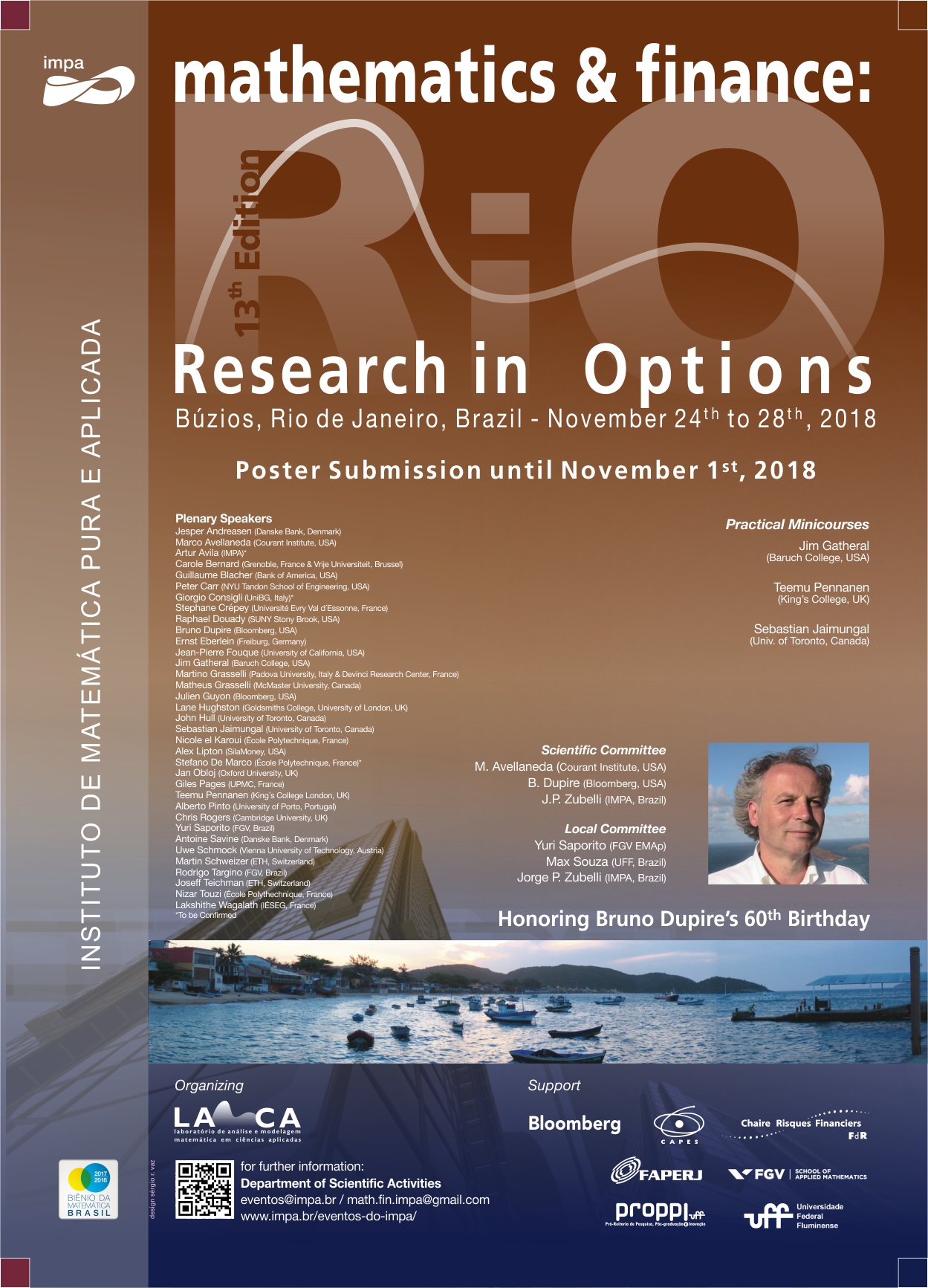

The RiO 2018 conference in mathematical finance, organized by IMPA, was held in Buzios, Rio de Janeiro, Brazil, on 24-28 November 2018, to celebrate the 60th birthday of Bruno Dupire, one of the most influential figures in the history of financial derivatives. The event gathered a number of leading scientists and professionals in one of the most productive and satisfying conferences of the year.

As one of his original alumni, I was given the responsibility to retrace some of Bruno’s ground breaking innovations, and, as a lecturer in Volatility, put them in perspective in the context of volatility modeling and derivatives trading.

See my slides here:

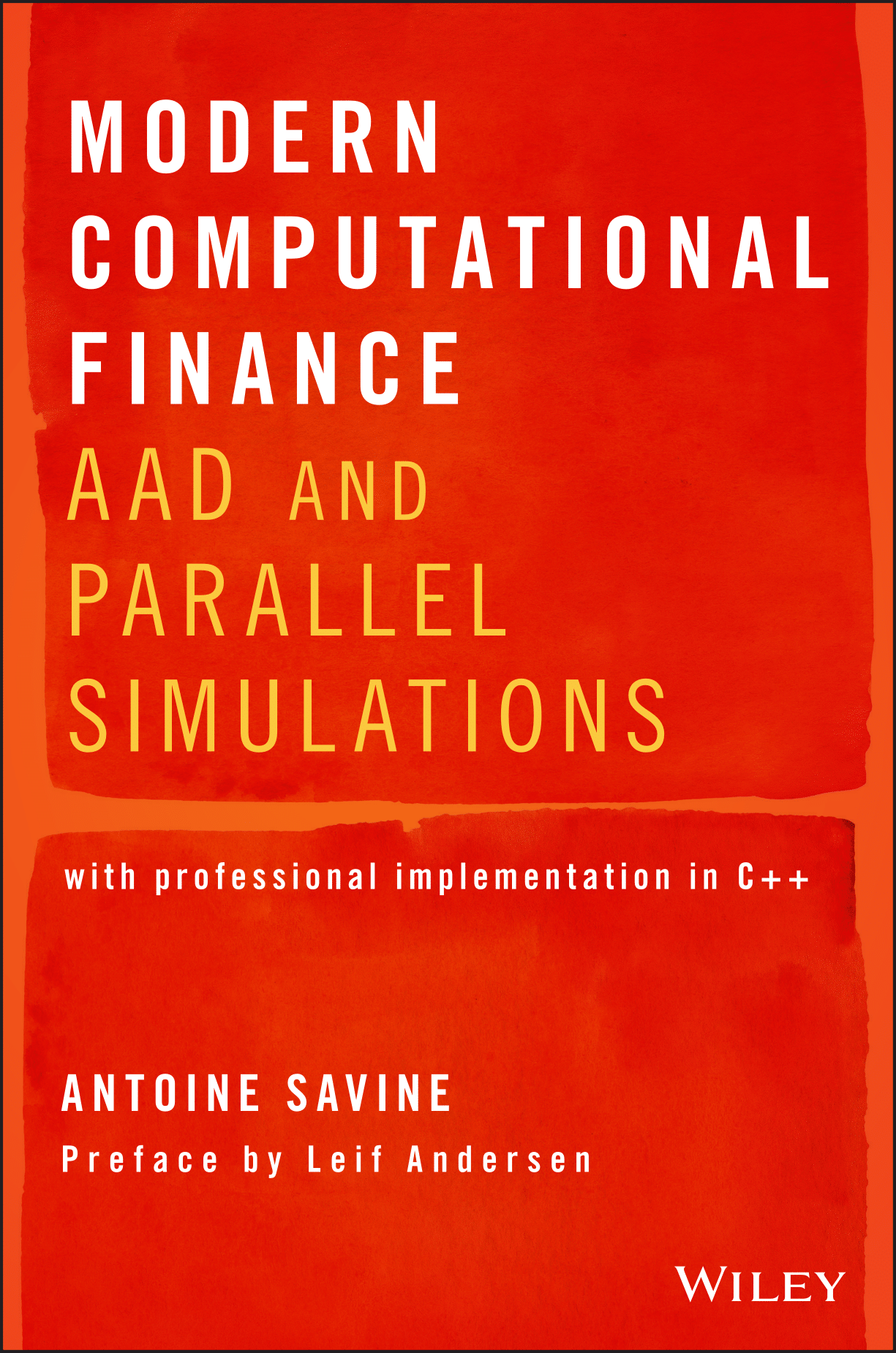

My book is out on Amazon today. You can read about it in my Medium post:

A free preview, including Leif Andersen’s preface, is available here:

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=3281877

The companion code is freely available on GitHub:

http://github.com/asavine/CompFinance/wiki

Follow the repo to be notified of updates, extensions and fixes.

I will be answering questions, suggestions and comments on my GoodReads page:

http://www.goodreads.com/author/show/18069638.Antoine_Savine

I put all my years of promoting, teaching and professionally implementing automatic adjoint differentiation (AAD) in this book, yet it took years of working nights and week-ends to (hopefully) get it right. I hope readers find that it was worth the effort.

Antoine Savine

Heading to Brazil next week to speak in the Rio 2018 event, honoring Bruno Dupire’s 60th birthday.

https://impa.br/en_US/eventos-do-impa/eventos-2018/research-in-options-2018/