Posts

60th birthday: a tribute to Bruno Dupire

The RiO 2018 conference in mathematical finance, organized by IMPA, was held in Buzios, Rio de Janeiro, Brazil, on 24-28 November 2018, to celebrate the 60th birthday of Bruno Dupire, one of the most influential figures in the history of financial derivatives. The event gathered a number of leading scientists and professionals in one of the most productive and satisfying conferences of the year.

As one of his original alumni, I was given the responsibility to retrace some of Bruno’s ground breaking innovations, and, as a lecturer in Volatility, put them in perspective in the context of volatility modeling and derivatives trading.

See my slides here:

Follow me on SlideShare

https://www.slideshare.net/AntoineSavine/presentations

For those of you who like my posts and stories, I am working on a few nice talks and workshops on introductory automatic differentiation, deep learning, Monte-Carlo simulations and parallel programming that will land on my SlideShare page soon. Please follow me to be notified of updates.

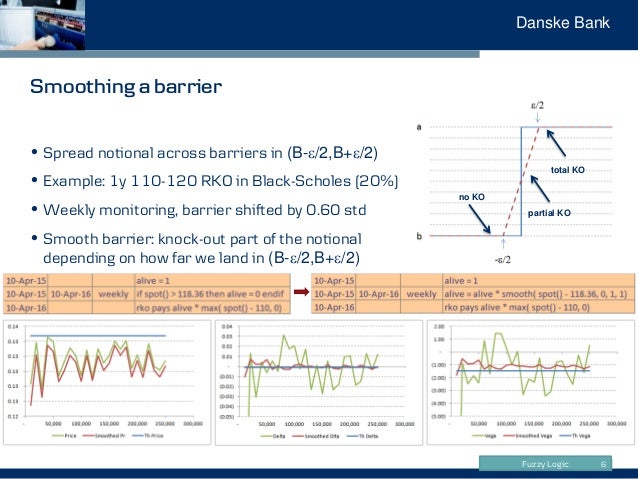

Right now, my page has my volatility lecture notes from Copenhagen University, my interest rate modeling slides from a course internal to Danske Bank, an introduction to multi-curve and collateral consistent discounting, some material on AAD and scripting, and a personal favorite about risk smoothing and fuzzy logic.

Comments, suggestions and questions are welcome, of course.

Modern Computational Finance: broken Amazon Kindle ebook

The Amazon Kindle version of the ebook Modern Computational Finance: AAD and Parallel Simulations by Antoine Savine is broken. The equations are wrongly rendered, making the ebook unreadable.

Amazon and Wiley have been notified and the ebook will be fixed soon on Amazon. Please do not purchase in the meantime. The ebook is also available on other places, like Apple Books or Wiley’s own store. (As far as we know) the ebook is only broken on Amazon.

Thank you for your patience.

Antoine Savine

Modern Computational Finance book pages

Please post your questions, suggestions, comments or reviews of the book Modern Computational Finance: AAD and Parallel Simulations on the author’s page:

https://antoinesavine.com/books-by-antoine-savine

or the book’s GoodReads page:

http://www.goodreads.com/book/show/40244920-modern-computational-finance

A public preview, including Leif Andersen’s preface, is available on SSRN: